Graphs pinched from Scott Sumner's blog:

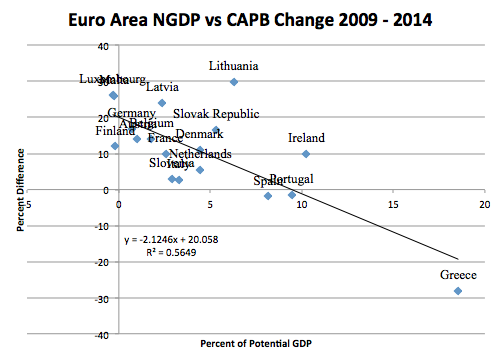

# Eurozone/no independent monetary policy -

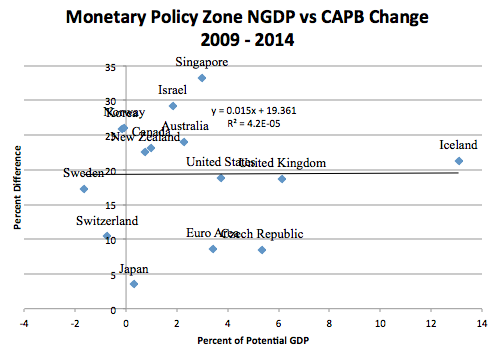

# Independent monetary policy -

Scott Sumner uses this result to claim support for the "Market Monetarist" position (that monetary offset is always possible and so there is no reason to use fiscal policy), over the Keynesian position (that monetary policy is exhausted when interest rates reach their ZLB and fiscal policy should be used). The application of this result to the UK might be that the combination of austerity (to eliminate the government's budget deficit) and expansionary monetary policy (to boost the economy) is a perfectly coherent and practical policy choice.

Is this a valid conclusion to draw? As Nick Rowe says "It's 6 days now, which is a long time in the blogosphere. I have seen posts about who said what about who said what. What I want to see are posts that interpret those correlations. And other interpretations/explanations are always possible (though econometricians bravely try to minimise the number of plausible interpretations). How would you explain them?"

I would guess that an important explanation here is relative devaluation: Using data from BIS, there is a strong negative correlation between the degree of austerity and the devaluation experienced for the floating rate countries. If devaluation is associated with economic expansion (which seems plausible), but under floating exchange rates devaluation occurs at the same time as fiscal austerity, then austerity could be ceteris paribus contractionary, but we would not see the actual contraction under floating rates - so e.g. in Iceland we see austerity (contractionary) and devaluation (expansionary) and overall not much impact. In Eurozone countries we see only the ceteris paribus contractionary effect of fiscal austerity.

The problem for the policy conclusions that you might draw if this is the explanation is that in times of depression, not everyone can devalue against everyone else - it is by definition a zero sum game. So devaluation worked well for Iceland which was small and could achieve lots of relative price movement against e.g. the US, but it cannot work in general. There's still a need for fiscal policy - especially in relatively large currency zones like UK (which is certainly large relative to the Icelandic Krona).

----------------------------------------------------------

Technical results:

# Regression for eurozone/fixed rate countries. Note negative and significant coefficient for degree of austerity (capb) upon economic performance (ngdp): point estimate = -2.12, p_value = 0.1%

# Regression for floating rate countries. Insignificant relationship (p_value = 88.4%) between degree of austerity and economic performance.

# Adding trade weighted exchange rate movement over the period (xrchg) changes the picture. The correlation between the capb and xrchg variables is -63%, and the observed variation in the combination of the two variables enhances the observed negative effect of austerity upon economic activity. The austerity variable is still not significant but its 95% confidence interval includes the point estimate for the fixed rate eurozone economies.

David: this is a good response.

ReplyDeleteIt is true that we can't have all countries depreciate their exchange rates. But if you see exchange rate depreciation as a *symptom* of (relative) monetary easing, that still leaves open the possibility that all countries could ease their monetary policies and offset fiscal tightening. (It doesn't prove it, but it doesn't disprove it.)

But your regressions are good, in that they help us understand better what is going on. Your results could have come out the other way, which would have forced a re-thinking of the interpretation.

If devaluation was central, to what extent would you expect the growth in those countries that did grow relatively well to be export-led?

ReplyDeleteThat could be a way of addressing, as Nick suggests, the problem of devaluation and monetary stimulus being correlated.

David, is your 3rd regression using the same set of economies/areas/countries as your 2nd one? What are the countries you use in all three regressions?

ReplyDeleteAlso, here's some criticism of using Iceland (basically the claim is that Iceland was not in a liquidity trap when it experienced "austerity").

Your thoughts?